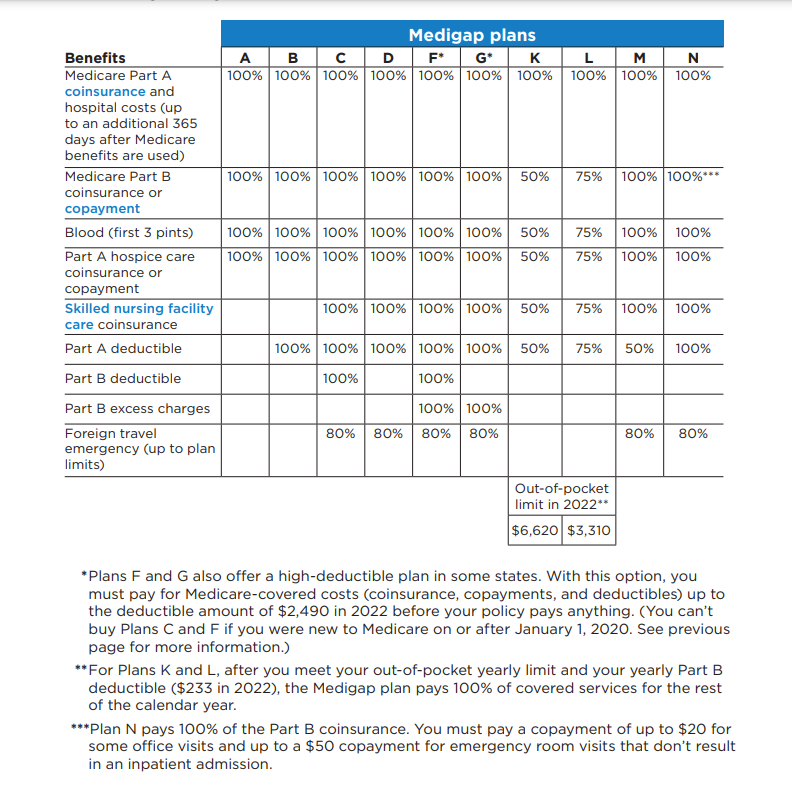

Every year Medicare publishes a guide to choosing a Medigap policy. Below is the Medicare guide for 2022.